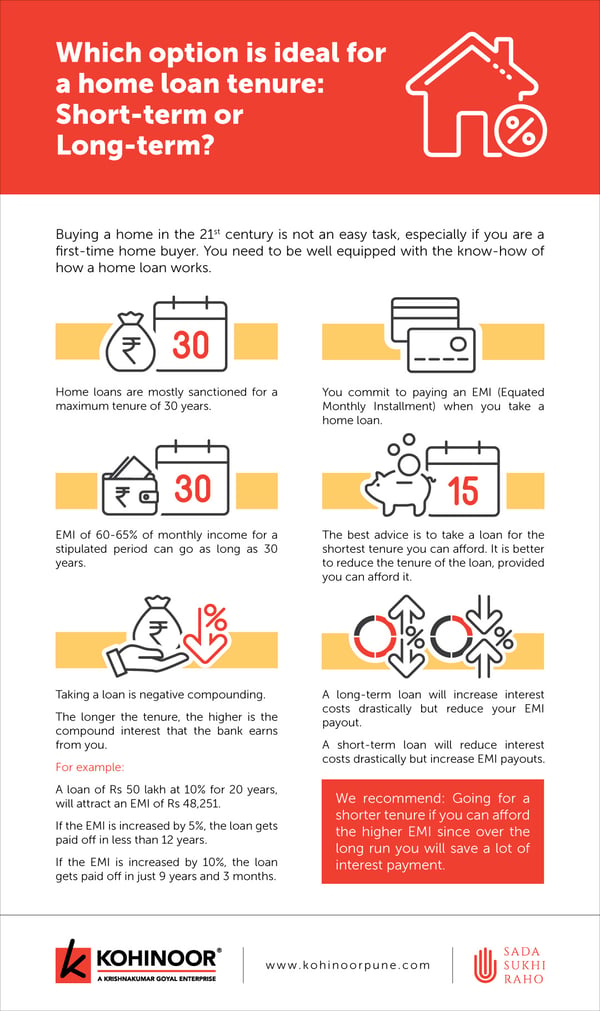

The quintessential Indian dream for a long time is of owning a home. However, buying one in the 21st century is not an easy task, especially if you are a first-time home buyer in particular as you will need to be well equipped with the know-how of how a home loan works.

So, let’s start with the basics

A home loan is usually taken either for the construction of a new house or renovation or to buy a flat/apartment. Moreover, the eligibility for the same generally depends on the repayment capacity and property price.

Furthermore, home loans are mostly sanctioned for a maximum tenure of 30 years, but it is observed that the average period people take to pay off their home mortgage entirely is around 8 years.

You commit to paying an EMI (Equated Monthly Installment) when you take a home loan. EMI of 60-65% of monthly income for a stipulated period can go as long as 30 years. The longer the tenure, the lower the EMI.

This might seem tempting for you to go for a 25-30 year loan. But, the best advice is to take a loan for the shortest tenure you can afford. Long-term loans lead to higher interest payments. So, it is crucial that you make the right choice that won’t hurt you in future.

Generally speaking, home loan terms can include 10, 15, 20, 25 and 30-year loan terms. 25 and 30-year loan terms are the most common, with 10 and 15-year loan terms generally being confined to interest-only repayments.

Shorter the loan tenure the Better for you!

By default, a bank offers the option of lowering the tenure of the loan. This is because any change in the EMI requires additional paperwork.

In fact, “Even in the clients’ interest, lowering the tenure is a better option,” says Vipul Patel of Home Loan Advisors. The choice of lowering the EMI and keeping more money in hand may sound tempting. But it is best to reduce the tenure of the loan, provided you can afford it.

The longer the tenure, the lower is the EMI, which makes it very tempting to go for a 25-30 year loan. In a 10-year loan, the interest paid is 57% of the borrowed amount. This shoots up to 128% if the tenure is 20 years.

If you take a Rs 50 lakh loan for 25 years, you will pay Rs 83.5 lakh (or 167%) in interest alone. “Taking a loan is negative compounding. The longer the tenure, the higher is the compound interest that the bank earns from you,” warns financial trainer P.V. Subramanyam. (Source: Economic Times)

Increasing the EMI amount can have a dramatic impact on the loan tenure. Assuming that the borrower’s income will rise 8-10% every year, increasing the EMI in the same proportion should not be very difficult.

If a person takes a loan of Rs 50 lakh at 10% for 20 years, his EMI will be Rs 48,251. If he increases the EMI every year by 5%, the loan gets paid off in less than 12 years. If he tightens the belt and increases the EMI by 10% every year, he would pay off the loan in just 9 years and 3 months.

Related Post - How to Save Tax on Real Estate Investment?

Fixed Interest Rate Home Loan

It is a type of home loan rate, wherein the interest rate is fixed for the entire tenure of the loan. This means you won't incur significant changes in the interest rates according to the economic market scenario.

Moreover, under this type of loan, in the beginning, a vital component of EMIs, go into servicing the interest whereas it is only in the latter half where the principal repayment comes in. The best part of this loan is that the interest rate remains the same throughout the tenure, which brings a level of certainty for the borrower.

Extremely convenient and helpful for good budgeters because it comes with a fixed monthly repayment schedule.

Related Post - Benefits of adding your spouse as a co-owner when buying a home

Floating Interest Rate Home Loan

A type of home loan where the rate of interest will vary depending on the market conditions. So, meaning that the interest rate might go up or down, depending on the market performance. However, it is comparatively cheaper than the fixed interest rate home loans, as long as the market remains stable.

Finally, a longer tenure will increase interest costs but reduce EMI payout. A shorter tenure will reduce interest costs but increase EMI payouts. It is always recommended that you opt for a shorter tenure if you can afford the higher EMI since over the long run you will save a lot of interest payment.

Related Post - What is the Procedure for Applying for a Home Loan?

comments